Global AML Compliance Automation

The iComply Promise

- Mitigate AML & CFT Risk

- As Low as $1 per Client per Year

- Streamline KYB, KYC, KYT Operations

- Boost Efficiency & Effectiveness

- Improve Customer Satisfaction

Start a risk-free trial of iComply today.

Trusted by AML Compliance Leaders Worldwide

iComply Platform Modules

One Platform. One Login. Global Compliance.

KYB

for Corporates

Onboard, verify, review, refresh, and reporting for legal entities

Click to Learn More

KYC

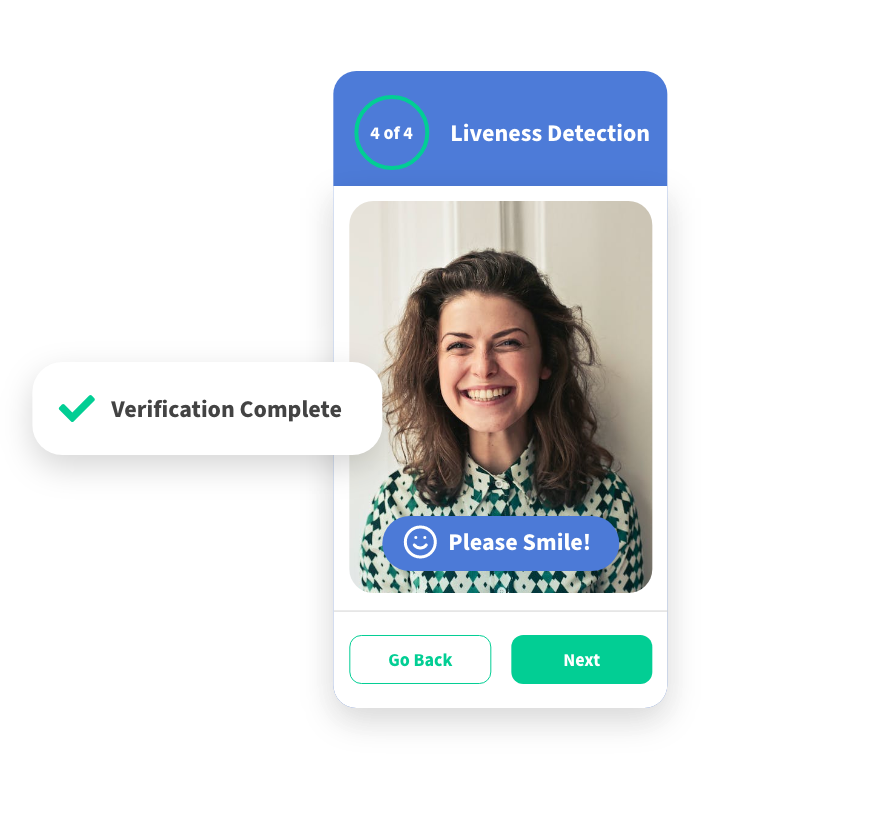

for Individuals

Identity verfication and fraud detection for natural persons

Click to Learn More

KYT

for Transactions

Batch processing and real-time transaction monitoring

Click to Learn More

AML

Risk Screening

On-demand or continuous monitoring for AML/CFT risk

Click to Learn More

Start your free trial of iComply

Cancel Anytime. No Questions Asked.

Compliance Failures Cost Time, Money, & Trust

Disjointed Vendors

Complicates operations, drains development resources, and introduces risk

Manual Processes

Limits growth, requires excessive workforce resources, and increases human error

Negative Customer Experiences

Erodes trust, brand value, and competitive advantage

Streamlined AML Software for KYB, KYC, & KYT

Eliminate Vendor Complexity

Create your ideal solution – Deploy our turn-key AML software in days or request customizations unique to your requirements

Boost Efficiency & Effectiveness by up to 90%

Configure intuitive workflows and automation to apply your policies and procedures at scale

Improve Customer Satisfaction by over 25%

Offer a white-glove customer experience using our white-labelled onboarding portals

World-Class Privacy, Security, & Encryption

Adhere to data protection regulations including SOC2 and ISO 27001, CCPA, GDPR, PPIA, PIPEDA, PCI, and more.

Process and secure all sensitive data, documents, and biometrics on the user’s own device, not our servers, using the power of edge computing.

Leverage best practices with end-to-end encryption (TLS1.2, SSL, AES256) to store member data on your servers or clouds.

Global AML Compliance

Streamline and automate compliance in 195 countries.

14,000+ Identity Verification Documents

3,000+ Watchlists for Sanctions Screening

11,000+ Trusted Sources for Adverse Media Checks

PEPs Class 1-4: Politically Exposed Persons

We have settled in with your service and are very impressed. I have every confidence in iComply for the UK, where increasing pressure from regulators to not only improve AML compliance, but also to be able to demonstrate it.

Frequently Asked Questions

Learn more about about AML compliance, customer due diliegnce, and how iComply can support your business

Start your free trial of iComply

Cancel Anytime. No Questions Asked.